Gold vs. Stocks as Inflation Hedge

February 26, 2026

Beginner

While the S&P 500 has won over five decades, gold has dominated during periods of extreme inflation and geopolitical turmoil. Conditions and time horizon matter.

It's practically an article of faith among some investors: Since the United States abandoned the gold standard more than 50 years ago, the precious metal has been viewed as a hedge against inflation and the "debasement" of "fiat" (government) currencies issued by central banks. And over the past half-century, gold prices have risen much faster than the Consumer Price Index (CPI)—the most closely watched measure of inflation. But gold isn't the only way to hedge a weakening U.S. dollar—and it might not even be the most effective. Some investors point instead to stocks.

The chart below shows the percentage gains for Gold futures (/GC), the S&P 500® Index (SPX), and the CPI from January 1975 through January 2026. Gold prices clearly outpaced inflation, but the SPX beat both gold and inflation.

Source: thinkorswim® platform

For illustrative purposes only. Past performance is no guarantee of future results.

But for very long periods within that 50-year stretch, the results were different. Inflation, as measured by the CPI, and stocks rose much faster than gold for about two decades (roughly 1980 to 2001), while gold rose much faster than both stocks and inflation in the decade that followed (roughly 2001 to 2011).

Gold's long decline

The chart below highlights 1980 through 2000. Gold clearly didn't preserve purchasing power during this period as its price fell nearly 60%, even as the Federal Reserve ushered in the "great moderation" of lower and more stable inflation starting in the early 1980s.

Source: thinkorswim platform

For illustrative purposes only. Past performance is no guarantee of future results.

What explains gold's dismal performance over this period? For one thing, late 1979 marked the end of an astonishing run for gold prices, capped by the kind of parabolic move that, regardless of market, often results in a long drift lower. Meanwhile, 1982 marked a major long-term turning point for U.S. equities, which had been in a secular bear market for the previous 14 years. This jumpstarted an historic 18-year run on the SPX.

Conditions turned less favorable for gold in the 1990s. During most of that decade, the Fed maintained relatively high real interest rates (the nominal rate minus the inflation rate). In other words, investors could get relatively high "risk-free" returns on bonds. And stocks went on a tear in the second half of the decade. Gold became an afterthought for many.

"Gold prices lagged inflation at this time due to better opportunity costs in other markets," said Michael Zarembski, director of futures trading at Schwab.

Zarembski also noted that the United States pursued a strong dollar at this time, making most commodities more expensive to overseas buyers. This usually weighs on demand.

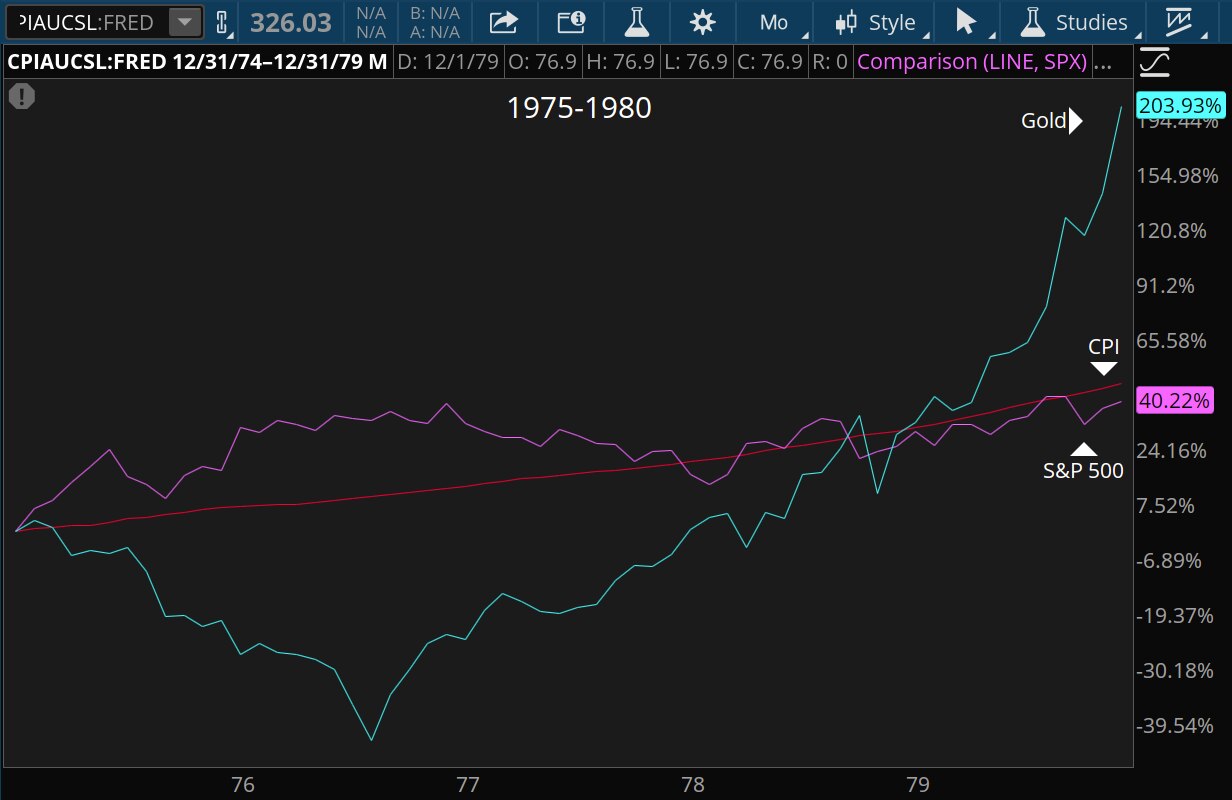

The '70s inflation shock

The chart below covers the second half of the 1970s, a period in which conditions favored gold, which more than tripled over a few years, far outpacing stocks and even soaring inflation. Gold tends to perform better during times of extreme or unexpected inflation, as well as heightened geopolitical volatility, according to Zarembski. And the 1970s had both. War in the Middle East led to the Arab oil embargo in the early 1970s. This led to soaring oil prices and inflation, which peaked at 13% in 1979. U.S./Soviet tensions ran high, and the Iran hostage crisis put Americans on edge. This also benefited gold, while stocks languished.

Source: thinkorswim platform

For illustrative purposes only. Past performance is no guarantee of future results.

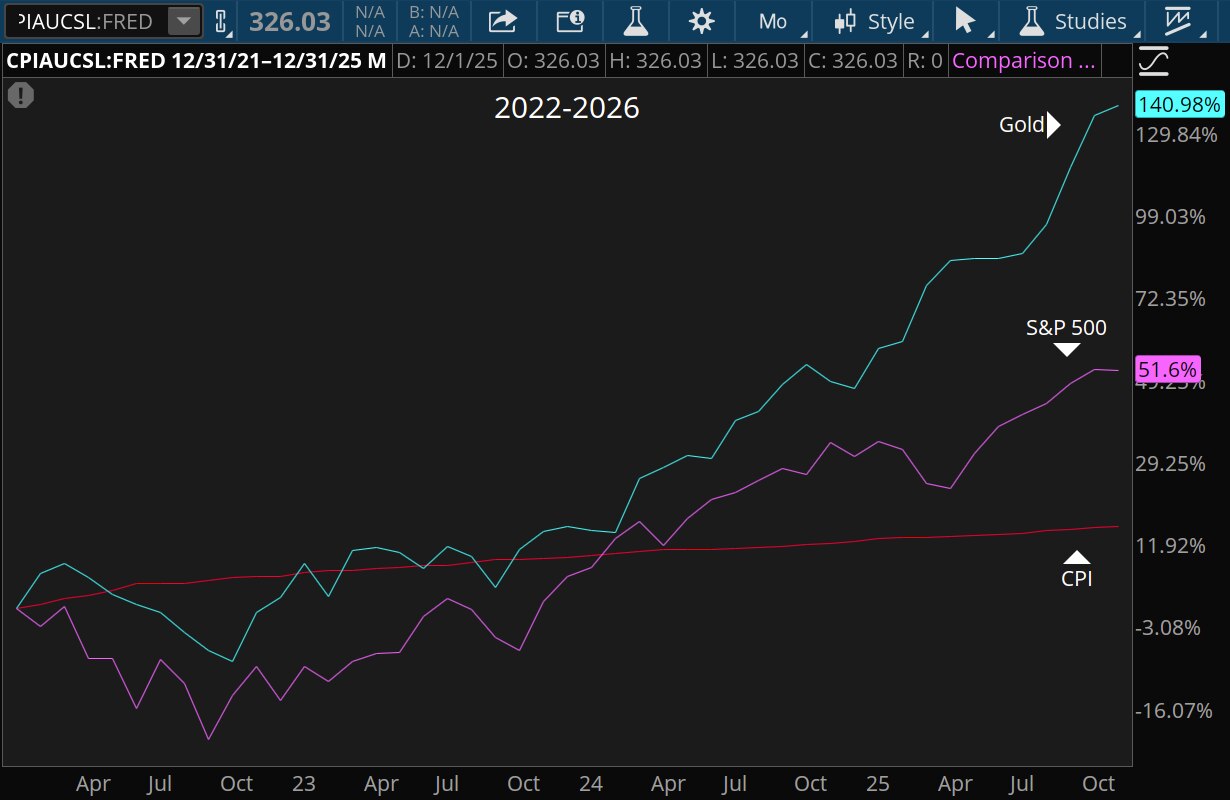

The chart below shows another incredible run for gold prices, this one more recent: Gold futures more than doubled in the two years through the end of 2025, easily outpacing the SPX and the CPI. The Covid-19-driven disruption to supply chains, and the resulting inflation shock of 2021–2022, rattled investors who had become complacent about inflation. The Fed still hasn't quite tamed inflation, leaving many investors concerned about a flare-up.

Meanwhile, surging government debt and the return of geopolitical uncertainty during the second Trump presidency are among the factors driving investors into gold. That includes central banks, which have bought unusually high amounts of gold in recent years to diversify their holdings from the U.S. dollar following sanctions and asset freezes after Russia's 2022 invasion of Ukraine.

Source: thinkorswim platform

For illustrative purposes only. Past performance is no guarantee of future results.

Bottom line

So, what's the better inflation hedge: gold or stocks?

Over the past five decades, the SPX clearly won the race, and there's a strong argument to be made for holding stocks instead of gold. Zarembski noted that companies have ways of maintaining margins as input costs rise, including by raising prices. But stocks serve as an effective hedge until inflation reaches extreme levels, at which point they tend to falter.

Time horizon matters. So do economic and geopolitical conditions. Five decades is likely a longer time horizon than most investors are planning for. The charts above illustrate that for long periods—many years at a time—gold has outpaced equities.

Over shorter periods, outcomes can differ drastically. Not all stocks or sectors perform well, and gold prices can drift lower for years at a time. Given that variability, and the limits of past performance, many investors emphasize diversification and continue to monitor market conditions.