Stocks Retreat on Oil, Iran to Start a Packed Week

July 13, 2026

Mounting attacks over the weekend in the Strait of Hormuz sent stocks, especially tech, down in early trading as oil rose. Tomorrow brings CPI, Warsh testimony, and bank results.

Published as of: July 13, 2026, 9:11 a.m. ET

Listen to this update

Listen here or subscribe to the Schwab Market Update in your favorite podcast app.

| The markets | Last price | Change | % change |

|---|---|---|---|

| S&P 500® Index | 7,575.39 | +31.75 | +0.42% |

| Dow Jones Industrial Average® | 52,637.01 | +149.60 | +0.29% |

| Nasdaq Composite® | 26,281.61 | +74.72 | +0.29% |

| 10-year Treasury yield | 4.58% | +0.01 | -- |

| U.S. Dollar Index | 100.92 | -0.02 | -0.02% |

| Cboe Volatility Index® | 16.40 | +1.37 | +9.12% |

| WTI Crude Oil | $74.42 | +$3.01 | +4.23% |

| Bitcoin | $62,700 | -$1,385 | -2.16% |

(Monday market open) After a weekend of strikes by both sides in the Strait of Hormuz that slowed tanker traffic to a crawl and sent crude oil prices surging, risk-off sentiment dominated Wall Street early Monday. This showed up in chip stocks as newcomer SK Hynix (SKHY) plunged 9%. Indexes fell across the board, and the tech-heavy Nasdaq trailed the pack.

Earnings lighten today before tomorrow's full court press when key banks step to the line before Tuesday's open. Results might bounce for the finance giants, analysts said, though Federal Reserve policy and economic uncertainty could make guidance interesting. Results from chip market barometers ASML (ASML) and Taiwan Semiconductor Manufacturing (TSM) loom later this week and provide clues into hyperscaler AI demand. A sliver of evidence emerged this morning as TSM—in a preview of its full report—said quarterly revenue climbed 36% annually, including a 68% jump in June alone.

Major indexes rose Friday ahead of the data and earnings barrage, lifted by mega caps and the U.S. trading debut of SK Hynix. Ten of 11 S&P 500 sectors advanced, continuing the broad rally. Volume remained below average, however, which might raise questions about conviction as the S&P 500 Index nears its all-time high set in June. Tech led all sectors last week, with the previous rotation toward cyclicals fading slightly as Magnificent Seven stocks took back the driver's seat, at least momentarily.

To get the Schwab Market Update in your inbox every morning, subscribe on Schwab.com.

Three things to watch

- CPI, Warsh converge tomorrow: Fittingly, perhaps, June's Consumer Price Index (CPI) data is due at 8:30 a.m. ET tomorrow, about an hour before Fed Chairman Kevin Warsh makes his semi-annual appearance before the House Committee on Financial Services. Monthly CPI is seen down 0.1%, benefitting from lower oil prices in June, while core CPI excluding food and energy expected to rise 0.2%. The key year-over-year core number is seen at a relatively benign 2.9%, though still well above the Fed's 2% goal. CPI is heavily weighted toward housing, where prices rose again for existing homes last month. The Fed likely takes this into account and looks more closely at Personal Consumption Expenditures (PCE) prices due later this month. "Is the peak of the recent inflationary impulse behind us? That's the question," said Collin Martin, head of fixed income research and strategy at the Schwab Center for Financial Research (SCFR). "An upside surprise poses a risk to our Fed view, and stronger underlying inflation would likely increase the likelihood of a rate hike." As of this morning, chances of a July 25-basis point rate hike were 33% and a September one at 69%, according to the CME FedWatch Tool.

- War distracts from earnings…again: President Trump's declaration last week that the ceasefire is "over" after Iran's attacks on shipping, and the subsequent escalation of tensions shifted attention back to an arena companies can't control. Unless this flare-up is brief, earnings calls in coming weeks may again focus on the potential impact of higher oil and yields and distract from the corporate growth outlook. Taking a broad view, S&P 500 earnings growth is seen strong in the second quarter, with FactSet pegging S&P 500 almost 24% annually. However, that includes more than 60% projected annual growth for the info tech sector, meaning expectations are very high in that one sector approaching the green flag and concentration of earnings growth in the largest names could remain a risk. Six of 11 S&P 500 sectors are expected to report earnings growth of less than 10%—more evidence of market bifurcation. Also, strong earnings can put more pressure on the Treasury market, where yields climbed last week to near recent highs, raising concerns about the cost of borrowing. Yields move the opposite direction of Treasuries. Twenty-eight S&P 500 companies report this week, including Netflix (NFLX).

- Whisper game: When earnings season gets rolling, it's common practice to watch revenue and earnings per share numbers to see if they met analysts' average estimate. This time around, meeting or topping consensus might not be enough to support shares, especially in the tech sector. That's where the "whisper numbers" among market participants may shape trading more than any widely shared views from Wall Street firms. These "whisper" numbers come from the buy side, among participants who actively trade and don't publish estimates. Still, these whisper numbers project hopes and hype. "The expectations bar is being set much higher than the consensus sell-side estimates, and that sometimes can come into play in terms of what the stock does," said Liz Ann Sonders, chief investment strategist at SCFR, in her most recent On Investing podcast. "So that's something I'm going to keep a close eye on." Sonders also said the margin story is big this quarter, especially with memory stocks posting huge margins. One possible rub for those firms is that someone is paying the higher price, likely their customers, which ultimately can lead to competition and possible loss of market share.

On the move

- SK Hynix, which competes with Micron (MU) in the memory sector, was listed temporarily as SKHYV on the Nasdaq Friday with a $1 trillion market capitalization. It surged 13% on its first day but tumbled sharply this morning following a sharp pullback overnight in the South Korean market.

- Other memory chip stocks including Micron and Sandisk (SNDK) fell 4% in early trading, keying off the South Korean market weakness. South Korea is sensitive to oil prices, with little domestic production of the commodity.

- Other chip and AI infrastructure stocks also dropped in today's risk-off trading, with shares of Applied Materials (AMAT), Intel (INTC), and Arm Holdings (ARM) off 2% to 3%.

- Crude oil surged early Monday. Tehran targeted U.S. facilities in multiple Gulf countries and declared the strait closed, and the U.S. hit 140 targets in Iran and said the strait is open. President Trump told Fox News this morning the U.S. will take over the strait and be its "guardian."

- Staples and health care stocks were among the early gainers this morning, along with energy companies, as investors adopted a defensive stance and watched oil prices. Materials stocks could come under pressure from gold and silver being down 1% and 2%, respectively, hit by the renewed Middle East tensions and concerns the Fed might keep rates high.

- Shopify (SHOP) rose 3% following an upgrade to buy from hold at Jefferies. The analyst cited third party data indicating Shopify's results could beat consensus estimates.

- Last week, the DJIA slipped 0.5%, the SPX advanced 1.23%, and the Nasdaq rose 1.74%. This ended a four-week winning streak for the DJIA but was the second straight winning week for the SPX, perhaps a sign that the mega-cap tech stocks have started to flex their muscle.

- Checking technical matters, the Nasdaq Composite and PHLX Semiconductor Index (SOX) both closed above their 50-day moving averages for a second straight session Friday, though SOX remains about 10% below its June peaks. Closing above those lines could suggest a constructive technical climate. Another dip below could trigger selling.

More insights from Schwab

Bear test passed for bitcoin? With bitcoin down about 50% from last October's peak and roughly $1.2 trillion in capitalization lost, it's time to ask if the pain is over or will persist. Part of this is confirming capitulation, but that's not easy. Read more about bitcoin's current and past bear markets, including how and why the old ones ended, in Schwab's new crypto piece.

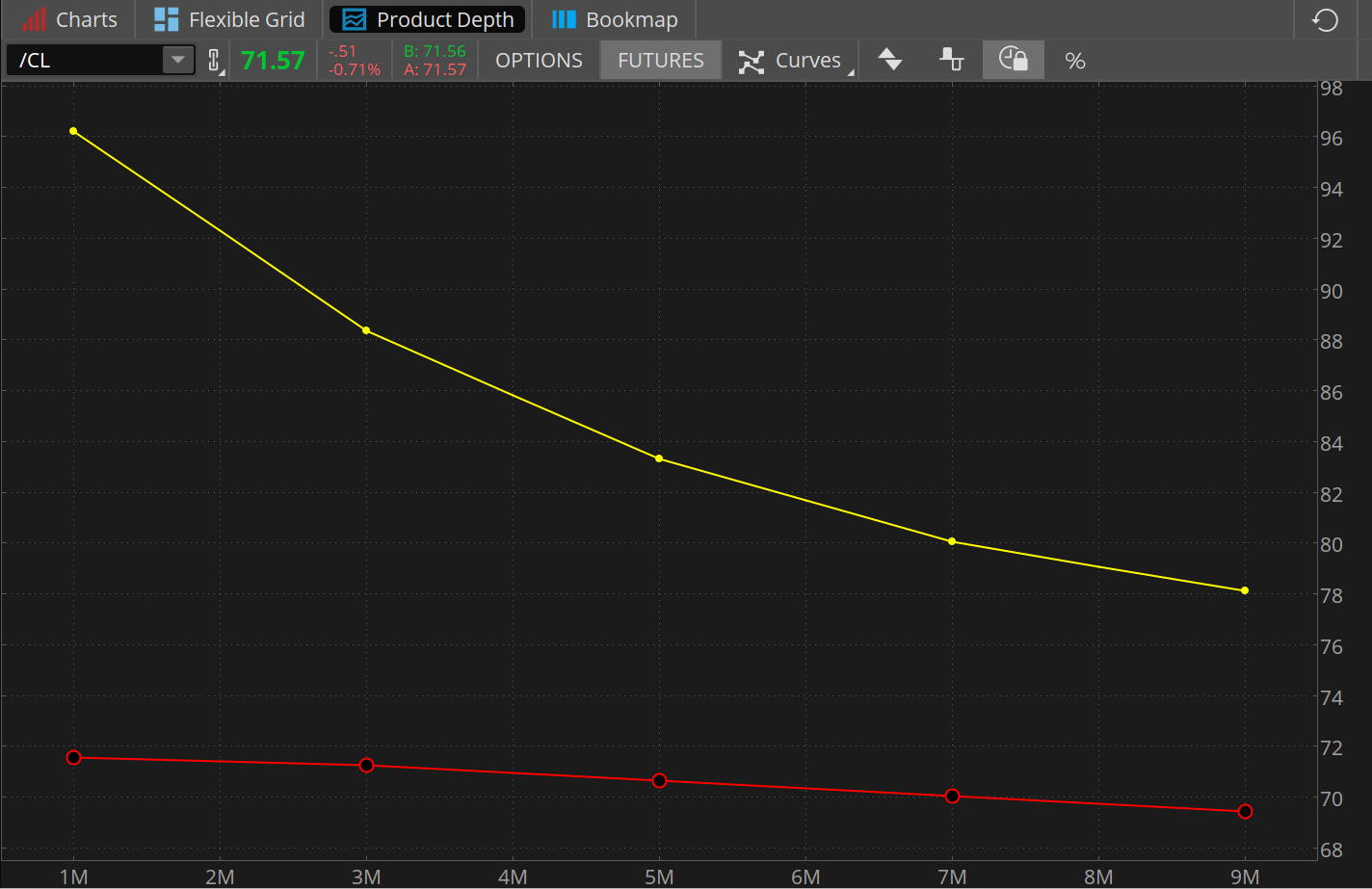

Chart of the day

Data source: CME Group. Chart source: thinkorswim® platform.

Past performance is no guarantee of future results.

For illustrative purposes only.

The CME crude oil futures market sees crude (red line) remaining right about where it is looking out over the next nine months, dropping to just below $70 by next spring from the current level near $71 per barrel. That's a different looking chart from two months ago (yellow line) when the market saw crude dramatically dropping from what then were very elevated levels. Crude ended up falling more quickly and sharply than the market anticipated, perhaps why dramatic drops aren't showing up now in forward contracts.

The week ahead